The views expressed in these remarks are those of the speaker in his role as FSB Secretary General and do not necessarily reflect those of the FSB or its members.

Good morning, everyone.

It is a privilege to join you today at Insurance Europe’s 16th International Conference. I’d like to thank Frédéric de Courtois for his thoughtful opening remarks and Insurance Europe for the opportunity to address such a distinguished audience of global leaders and regulators.

The theme of this year’s conference, “Building Resilience in an Uncertain World,” could not be more timely. We are currently facing profound shifts in our global landscape, including geopolitical, economic, and environmental. These changes bring with them both challenges and opportunities, and they underscore the critical importance of resilience, particularly in the financial and insurance sectors.

Today, I will share my perspective on the current geopolitical and economic outlook, the evolving risks we face, and the pivotal role the insurance sector can play in strengthening global resilience.

The current outlook

Let me begin by addressing the broader context in which we operate.

The ongoing conflict in Iran has introduced a significant degree of uncertainty into the global economic outlook. The disruption to the supply of oil and other commodities has led to higher and more volatile energy prices, raising concerns about a stagflationary shock to the global economy. This, in turn, has fuelled bond market volatility, as inflationary pressures impact investors’ expectations of central bank rate increases. While the current effects are macroeconomic, the ultimate impact on financial stability will hinge on the duration and severity of these disruptions to commodity supplies and global markets. The FSB is closely monitoring these developments for any indications of strain in the resilience of the global financial system.

At the same time, financial markets appear to be overly optimistic given the uncertain economic and geopolitical backdrop. Overvalued and stretched asset prices leave markets vulnerable to sharp downward adjustments, and we’ve already witnessed corrections in certain segments. For instance, bond markets have seen significant movements as concerns about inflation and sovereign debt levels have come to the fore.

Such volatility has the potential to exacerbate existing vulnerabilities in sovereign debt markets, where risks are already elevated. Heightened investor concerns about debt sustainability could further exacerbate refinancing challenges for governments. As we’ve seen in past episodes, stress in sovereign debt markets can spill over into the broader financial sector, amplifying risks to financial stability.

The increasingly interconnected nature of the global financial system means that vulnerabilities in one area can quickly propagate to others and can do so in new ways. This underscores the importance of vigilance, coordination, and proactive risk management to ensure that the financial system remains resilient in the face of evolving challenges. Let me share a few areas that the FSB is watching particularly closely.

Vulnerabilities related to sovereign debt markets

Firstly, sovereign debt markets are increasingly vulnerable due to the growing prevalence of leveraged bond trading strategies. These strategies are employed by some hedge funds looking to profit from arbitrage opportunities in government bond prices and associated derivatives. As highlighted in our recent report on Vulnerabilities in Government Bond-backed Repo Markets, hedge fund cash borrowing in repo markets has increased over the past few years, and now amounts to almost $3 trillion, or 25% of their assets. If the strategies face rising repo rates, higher haircuts or increased margin requirements, they could be unwound quickly, with destabilizing effects on markets during periods of stress. Similar dynamics contributed to significant market dislocations in March 2020.

These developments underscore the importance of maintaining robust risk management practices and ensuring that sovereign debt markets remain resilient in the face of rising challenges.

The insurance sector also has an important role to play in managing these risks. Insurers are significant investors in sovereign debt, and their investment decisions can have a meaningful impact on market dynamics. Insurers, with their long-dated liabilities and structurally large allocations to sovereign debt, are well-positioned to act as patient, stabilising investors in government bond markets, a role of growing importance as other participants pursue shorter-horizon, leverage-driven strategies. Yet the stabilising function performed by long-term investors should not be assumed. For instance, the 2022 gilt market episode, which was driven primarily by pension funds and liability-driven investment strategies, illustrated a broader mechanism that may be relevant to institutional investors with significant fixed income exposures and derivatives overlays: under stress, collateral demands and margin calls can compel asset disposals at precisely the moment markets are most fragile, transforming a structural buyer into a source of amplification. While insurers operate under more stringent liquidity and capital frameworks, ongoing supervisory focus is necessary to ensure that the sector’s stabilising role in sovereign debt markets is durable. This includes areas such as collateral management practices, derivatives exposures, and liquidity preparedness under adverse scenarios, to ensure resilience during periods of market stress.

Vulnerabilities related to private credit

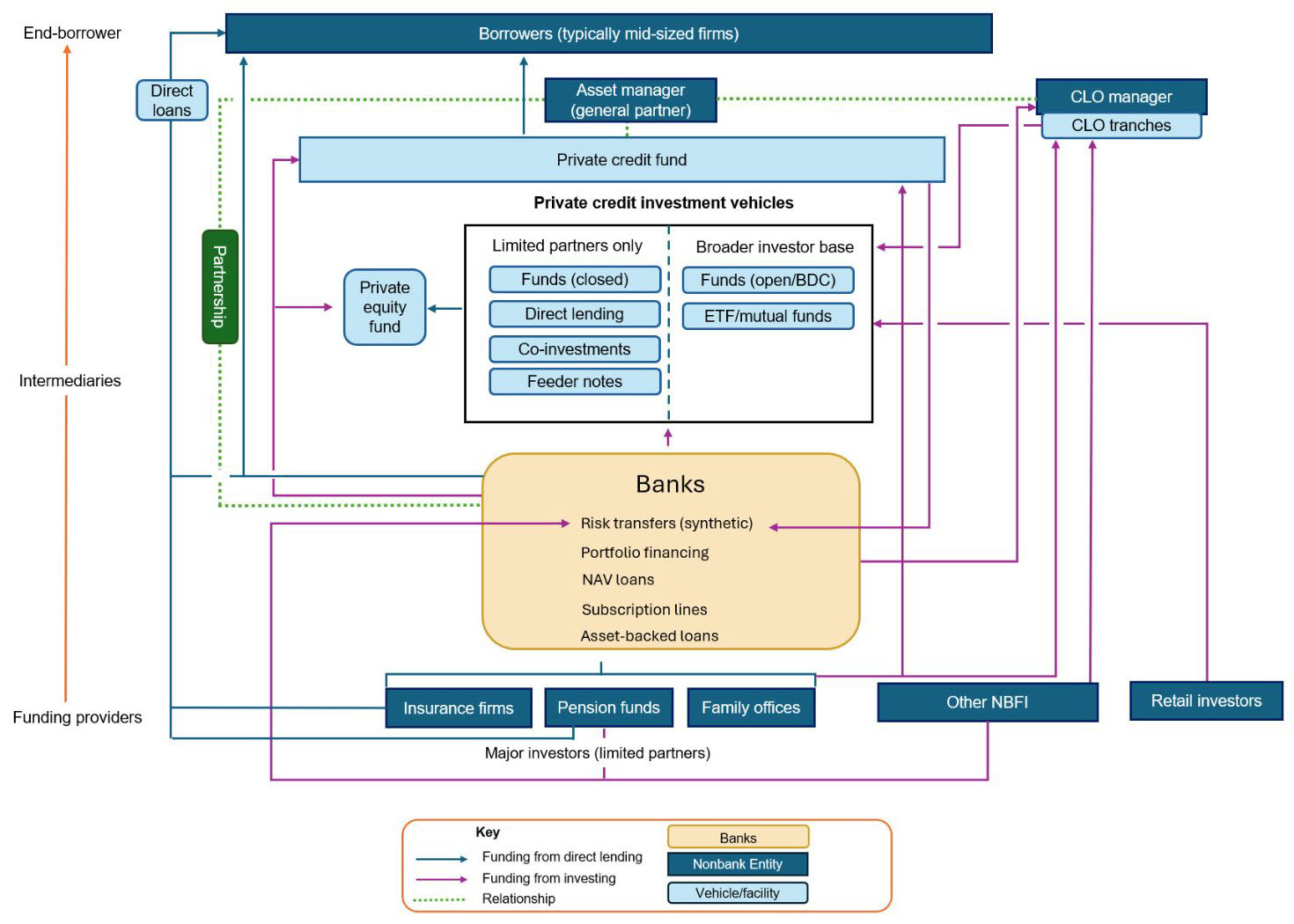

Let me turn to private credit. The FSB defines private credit as nonbank direct lending to medium-sized companies negotiated on a bilateral basis. This financing serves as a vital source of diversification and innovation in financial markets. It bridges critical financing gaps, offering solutions to companies that may be underserved by traditional banks or public markets. Private credit provides faster execution, more tailored structures, longer-term capital commitments, and greater flexibility for borrowers with complex or unconventional needs. It also plays a crucial role in supporting emerging industries, such as artificial intelligence, by providing the debt funding needed to fuel their growth.

The growth of private credit has been remarkable. In the past decade, the sector has expanded significantly, with total assets estimated between $1.5-2.0 trillion at end-2024, across the jurisdictions contributing to our assessment. However, some alternative estimates are much higher. Private credit is expected to continue growing as companies seek alternative sources of financing.

However, alongside these opportunities, private credit introduces a complex array of questions and vulnerabilities that warrant closer examination. Interconnections between private credit funds, banks, insurers, and private equity firms are deepening, raising concerns about potential spillovers in times of stress.

Our recent report on private credit highlights several key vulnerabilities arising from interlinkages with banks, borrower credit quality, and valuations. Importantly, the market remains untested at its current scale; and data gaps mean that authorities do not have full visibility and understanding of potential contagion propagation channels.

Our report also underscores the interconnectedness of private credit with the insurance sector. Insurers and pension funds are key investors in private credit with their activity in this asset class having grown recently. For example, insurers in multiple FSB jurisdictions have seen increasing investments in private assets, and certain large private defined-contribution pension funds and superannuation funds have increased their allocations to illiquid private equity and credit in recent years.

Private equity funds appear to be another key interconnection. Private equity sponsors typically back borrowers in private credit and also appear to be increasingly developing ownership or control relationships with insurers, which are then used to invest in private credit funds.

In addition, private credit issuers rely on private credit ratings that are sometimes provided by smaller and lesser-known agencies. The ratings are important, for example to some investors like insurers, but the use of lesser-known agencies has also raised questions.

A key feature of the above institutional interlinkages relates to cross-border aspects, driven by international capital flows and favoured by diverse market structures, exposing further potential vulnerabilities and channels of propagation of stress.

The concern is not private credit as an asset class, but rather with how private credit might behave under stress and the potential risks associated with that. Indeed, private sector leaders have also raised alarms about these vulnerabilities. Addressing these vulnerabilities will require greater transparency, improved data collection, and enhanced regulatory oversight.

The FSB has outlined follow-up work related to:

- deepening the analysis of interlinkages and potential vulnerabilities related to liquidity mismatch: This includes examining ties with private equity firms and insurers, and understanding potential issues related to liquidity mismatch in certain private credit funds.

- improving transparency in order to address data gaps, enhance reporting frameworks, and develop harmonised global definitions to support effective monitoring.

- sharing supervisory approaches in order to strengthen risk management and governance practices for both banks and nonbanks active in private credit, particularly around valuations and the use of private ratings.

The FSB work on the insurance sector

The insurance sector is not immune to these broader trends. In fact, it is uniquely positioned at the intersection of many of the challenges we face. I’ve mentioned some of these already, like the growing complexity of financial markets, but insurers may also be more directly exposed to challenges from climate change and aging populations than are other parts of the financial system.

One area where the insurance sector plays a particularly critical role is in addressing climate-related risks. The increasing frequency and severity of extreme weather events have highlighted significant protection gaps in many parts of the world. These gaps leave individuals, businesses, and governments vulnerable to the financial impacts of climate events.

Closing these protection gaps will require innovative solutions, including new insurance products, enhanced risk modelling, and greater collaboration between public and private stakeholders. The FSB will continue to support these efforts, including through our work on climate-related financial disclosures and our collaboration with the International Association of Insurance Supervisors (IAIS).

Another area of focus is the resilience of the insurance sector itself. The FSB, in partnership with the IAIS, has made significant progress in developing guidance relating to insurer resolution. In April, the FSB published its final guidance for authorities to assess which insurers should be subject to recovery and resolution planning (RRP) requirements. The guidance outlines six key criteria that authorities should consider: business model, scale, complexity, substitutability, cross-border activities, and interconnectedness. Additionally, it identifies specific circumstances in which recovery and resolution planning requirements should apply, such as when an insurer provides a critical function or when its failure is likely to have a material impact on the financial system and/or the real economy of the jurisdiction. This is intended to align with the requirements in the IAIS’s Insurance Core Principles.

Our decision to move beyond the Global Systemically Important Insurer (G-SII) framework, in favour of the IAIS’s holistic framework for assessing systemic risk in the insurance sector, reflects our recognition of the sector’s unique characteristics and the need for tailored approaches to addressing systemic risks.

Conclusion

In conclusion, while the challenges before us are undoubtedly formidable, they are far from insurmountable. The global financial system has shown remarkable resilience in weathering recent periods of market turmoil and stress, and I am confident that it possesses the strength to navigate the challenges of the present and future.

The insurance sector plays a critical role in fostering systemic resilience. Its ability to adapt to evolving risks and support economic stability is vital to a properly functioning financial system.

The FSB’s aim is to ensure that the sector remains robust and resilient, precisely because of its importance to the global economy. Insurance performs critical economic functions by pooling and transferring risk, mobilising long term savings into investment, and supporting financial stability. This, in turn, underpins confidence and continuity in the real economy, enabling households, businesses and governments to plan, invest and recover from shocks.

The FSB is committed to doing its part. We will continue to monitor developments closely and advance our work in key areas, including private finance and credit markets, foreign exchange derivative markets, and the growing complexity and interconnectedness of the financial system. We will also deepen our collaboration with the IAIS and other international bodies to ensure that the insurance sector remains a pillar of stability and resilience.

While the road ahead may be uncertain, it is also full of opportunity. As we confront today’s uncertainties, the need for resilience has never been greater. It is only through collaboration, vigilance, and innovation that we can address the challenges ahead. The insurance sector, with its unique capacity to manage risks and support economic stability, is an indispensable pillar of the global financial system. By working together across sectors and borders, we can ensure that our financial systems remain robust and adaptable, prepared not only to weather future shocks but to enable sustainable growth and prosperity for all.

Thank you.